2023 State of Accreditation Report

We are pleased to share insights we have gained from ����ý accreditation visits over the past academic year, providing ����ý members with a collective learning experience.

The continuous improvement experience that is a guiding principle for ����ý should be extended to everyone. This report curates the collective wisdom of our peer review visits, including outcomes, best practices, and future opportunities.

Have feedback? We want to hear from you!

2022–23 Accreditation Outcomes

Business Accreditation

Business Accreditation as of August 1, 2023

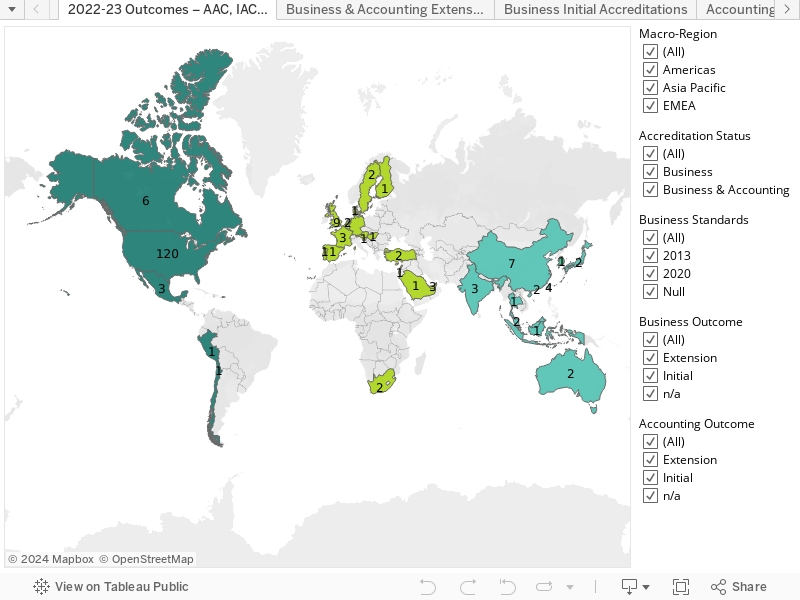

2022–23 Outcomes: AAC, IAC, CIRC Committee Meetings, July 1, 2022, Through June 30, 2023

Notes:

Data displayed are as of June 30, 2023. The outcomes map displays all initial accreditations and extensions of accreditation.

Total number of Extensions: 185 (includes business and accounting).

Total number of schools achieving business accreditation: 40.

Total number of schools achieving accounting accreditation: 2.

Initial Business Accreditation

Number of Schools in Process as of June 30, 2023

Initial Accreditation Visit Outcomes Between July 1, 2022, and June 30, 2023, Outcomes by Region

Continuous Improvement Review

Continuous Improvement Review Visits Between July 1, 2022, and June 30, 2023, Outcomes by Region

2022–23 Accreditation Insights

2020 Standards Mentioned

Schools With Visits Between July 1, 2022, and June 30, 2023, With Accredit and Extend Recommendations

Among both initial accreditation and continuous improvement review visits in 2022–23, the most frequently mentioned standards for schools to address by the next visit are standards 1, 3, 5, and 9.

Source: Peer review team reports.

Standard 1: Strategic Planning—Common Issues |

- Alignment of Mission With Practice: Schools face the challenge of aligning their stated missions with their actual practices and outcomes, and they are encouraged to reassess their missions in relation to their capabilities, distinctive assets, and core values.

- Strategic Planning: Schools are expected to demonstrate clear, comprehensive, and measurable strategic planning, with regular dissemination, monitoring, and assessment of the progress toward strategic objectives.

- Societal Impact: Schools are encouraged to clarify their societal impact focus and ensure alignment of this focus with the strategic plans of both the school and the university.

Standard 3: Faculty and Professional Staff Resources—Common Issues |

- Improvement in Faculty Qualification Management: Institutions are advised to improve their management of faculty qualifications and refine the faculty qualification process. Many schools are advised to review and revise their faculty qualification criteria to ensure they align with the ����ý standards as well as the school’s mission and strategies.

- Faculty Qualifications Ratio: Approximately one-third of schools visited last year did not meet the faculty qualifications ratio (Scholarly Academic + Practice Academic + Scholarly Practitioner + Instructional Practitioner) of 90 percent in one or more disciplines, indicating a need to improve faculty qualifications to meet ����ý standards.

- Faculty Deployment: Schools should monitor faculty qualifications and their deployment, particularly in light of high teaching loads, to ensure that faculty maintain their qualification status. Developing a strategy for administrative positions, including succession plans, is also essential to ensuring smooth transitions.

Faculty Insights

Faculty Qualification Ratios for Schools With Visits in 2022–23

Source: Table 3-1 data.

Faculty Sufficiency and Qualifications by Most Common Discipline

Participation Ratios by Discipline

SA Ratios by Discipline

to display by region, school size, and control.

Source: Table 3-1 data.

Commonly Reported Disciplines

- Accounting

- Business Law/Legal Environment

- Computer/Management Information Systems

- Economics

- Finance

- Management

- Marketing

- Quantitative Methods

The Profile That Emerges

Considering the insights above related to Standard 3, a profile of the ����ý schools visited in 2022–23 emerges: ����ý-accredited business schools visited in 2022–23 comprise faculty in traditional business disciplines, with a leaning toward quantitative disciplines. ����ý-accredited schools are composed of faculty who are overwhelmingly dedicated to the mission of the business school and engaged in all aspects of the business school that enable it to carry out its mission.

Standard 5: Assurance of Learning—Common Issues |

- Assurance of Learning (AoL) Process: Peer review teams note that AoL processes should be more refined and regularly monitored. Schools should better leverage data from a variety of sources. Institutions are also urged to involve faculty in the AoL process and align their processes with curricular changes.

- Implementation of New Programs: Institutions should conduct a critical analysis of AoL processes and learner success when introducing new programs. Review should include the budgetary implications, faculty sufficiency ratios, and enrollments of the new programs. Schools should similarly carry out an analysis of the curricular changes and the AoL processes related to the updated curriculum.

- Use of Direct and Indirect Measures: Institutions should use both direct and indirect measures in the AoL process. The 2020 standards require some indirect measures to be included in the overall AoL portfolio; thus, schools are encouraged to expand and more strategically leverage indirect measures to inform their curricular and programmatic changes.

Standard 9: Societal Impact—Common Issues |

- Developing a Mission-Driven Strategy for Societal Impact: Peer review teams note the lack of a comprehensive strategy for societal impact that aligns with a school’s selected focus area(s) and mission.

- Measuring Societal Impact: Schools should ensure that their societal impact efforts are directly aligned with their mission, vision, and strategic plans. The integration should be reflected in curriculum, internships, and other student activities.

- Developing Societal Impact Plans: The ����ý Initial Accreditation and Continuous Improvement Review Committees highlight the need for schools to focus on maturing their plans for societal impact, and it is therefore mentioned in virtually all decision letters sent to schools.

Insights

Looking across all visits under the 2020 standards, the recurring themes point to a need for schools to focus strategically and align faculty resources with the school’s mission. Schools should also analyze unsystematic risk so they are positioned for challenges that have a medium-to-high likelihood of occurring. The school’s mission should drive societal impact and thought leadership. Ensuring high-quality learning outcomes through assurance of learning continues to be an area of difficulty.

Supplemental Accounting Accreditation

Initial Accreditation and Continuous Improvement Review Accounting Visit Outcomes Between July 1, 2022, and June 30, 2023

Source: Peer review team reports.

Accounting Standards Most Frequently Mentioned for Visits Between July 1, 2022, and June 30, 2023

Standard A1: Accounting Academic Unit Mission, Impact, and Innovation |

- Strategic Planning: Accounting units are advised to pursue a more comprehensive strategic-planning process that involves key stakeholders including faculty, staff, students, and external affiliates. The units should also develop appropriate governance structures, such as a strategic planning committee consisting of various constituents, including accounting-specific stakeholders, for periodic review and plan updating.

- Technology Integration: Accounting units should consider enhancing the integration of technology and data analytics throughout the curriculum, both in undergraduate and graduate programs.

- Enrollment Strategies: Accounting units should develop strategies to increase undergraduate enrollments, especially in the context of declining accounting enrollments in certain parts of the world.

Standard A4: Accounting Curricula Content and Assurance of Learning |

- AoL Process Improvement: Accounting units are advised to mature and refine AoL processes, tracking broad-based measures of student success and impact and systematically assessing and utilizing data to inform program-level changes.

Standard A6: Accounting Faculty Sufficiency, Credentials, Qualifications, and Deployment |

- Faculty Qualifications: Accounting units should review and clarify faculty qualifications and scholarly academic criteria, ensuring that they reflect rigor consistent with the school’s mission, expected outcomes, and peer institutions.

In accounting, the most immediate issue involves strategic management, including managing declining enrollments of accounting degrees at both the undergraduate and graduate levels in certain parts of the world. As data analytics and related disciplines continue to gain momentum, accounting enrollments continue to decline, suggesting that accounting students may be choosing data analytics over accounting.

Undergraduate and Master's Accounting Degrees Conferred Between 2018 and 2023

Doctoral Accounting Degrees Conferred Between 2018 and 2023

Since 2020, there has been an increase in doctoral programs conferred.

Accounting Best Practice Example

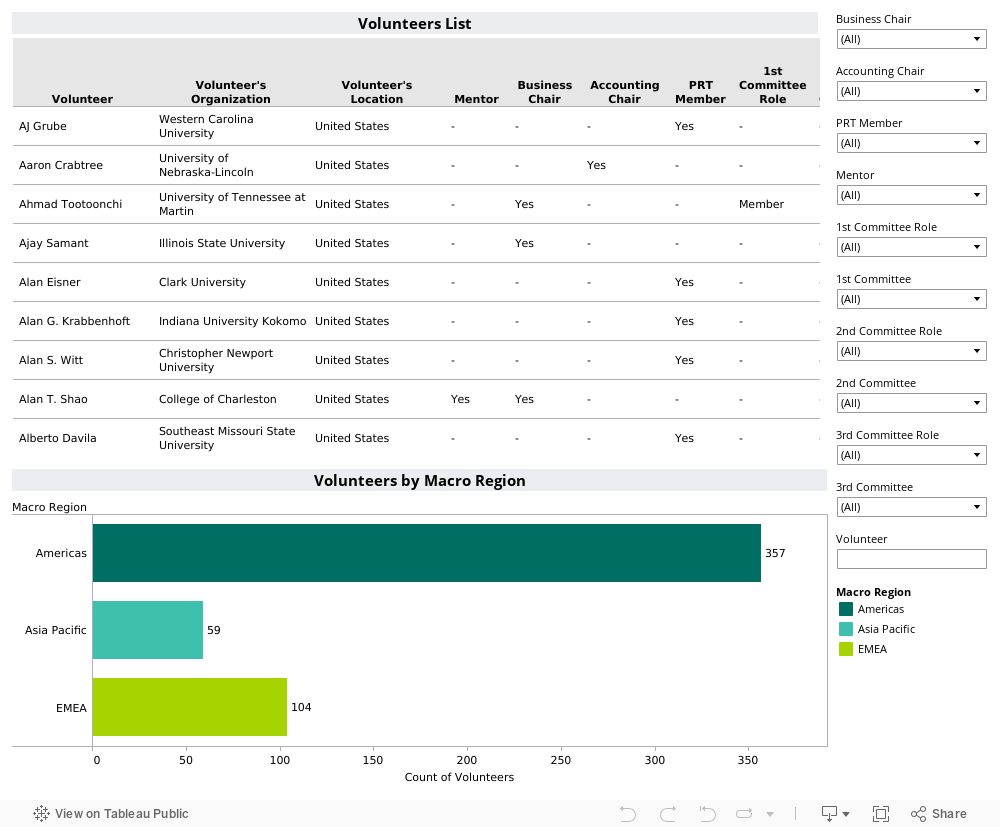

Volunteers

Volunteer Representation for 2022–23

Notes:

This list includes individuals who served as a volunteer between July 1, 2022, and June 30, 2023, in one of the following roles:

• Operating Committee Member (Accounting Accreditation Committee—AAC; Accounting Accreditation Policy Committee—AAPC; Business Accreditation Policy Committee—BAPC; Continuous Improvement Review Committee—CIRC; Initial Accreditation Committee—IAC)

• Mentor (business or accounting)

• Team Chair (business or accounting)

• Team Member (business or accounting)

Only individuals who agreed to be listed are included. If your name does not appear and you served on one of the roles listed above between July 1, 2022, and June 30, 2023, and would like to be added, please contact us at [email protected]. Thank you.

Satisfaction With Accreditation Experience

In 2023–24, ����ý will launch its volunteer refresher training course. Volunteers will be required to complete a refresher course every three years. The training will highlight key updates made since the release of the 2020 accreditation standards as well as lessons learned along the way from the perspective of peer review teams, committees, and accreditation staff.

Best Practices and Innovations

Top Areas for Best Practices Mentioned by Peer Review Teams

Best Practice Examples

Societal Impact

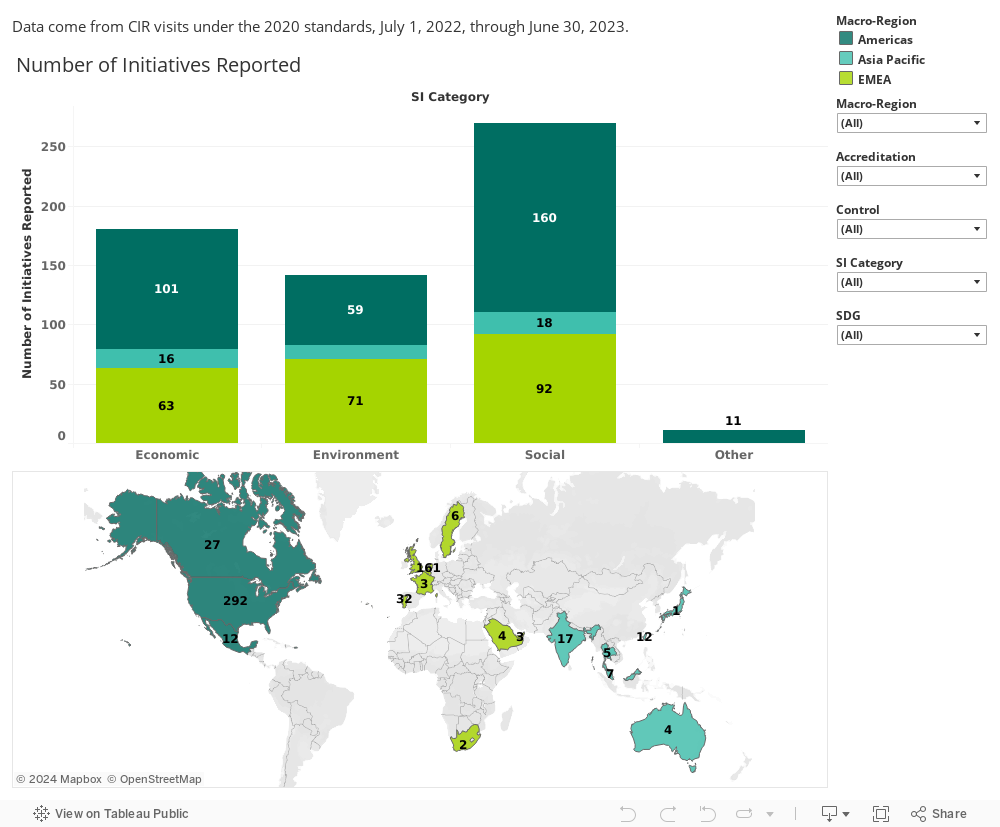

Societal impact is beginning to take shape as an important component of business education. Schools are leveraging the accreditation standards in this area to ensure that their programs and outputs contribute to solving some of society’s biggest challenges. Many schools use the United Nations Sustainable Development Goals (SDGs) as their framework for naming their focus area related to societal impact. Other schools use their own terminology or a different framework. To amalgamate reporting across different terminology, we categorize schools’ reporting into three broad types: economic, environmental, and social efforts.

Societal Impact Focus Areas

Initiatives Reported From CIR Visits Under 2020 Standards, Between July 1, 2022, and June 30, 2023

The data reveal that schools in Asia Pacific and EMEA are fairly evenly distributed among the three categories, while schools in the Americas place more emphasis on social and economic initiatives and less on environmental initiatives. Following are some exemplars of societal impact efforts in all three regions.

Looking Forward

New This Year

Many small and medium-sized schools do not have the resources to purchase third-party software to manage their accreditation reporting requirements. To aid schools with this effort, ����ý now provides comprehensive and easy-to-use Excel templates for the tables that must be submitted for accreditation reporting purposes (e.g., 3-1, 3-2, 5-1, etc.). These templates can be downloaded from the ����ý website.

What’s more, these tables can be uploaded into myAccreditation without having to save them in PDF format. Simply use the templates and upload each file as an Excel file. We hope these templates are a great value add to your school.

Artificial Intelligence (AI) and Accreditation

Generative AI is becoming ubiquitous in many aspects of our lives, and questions about the use of AI to facilitate accreditation visits and to prepare accreditation reports are occurring in everyday conversation. Just as the accreditation standards embrace a commitment to a growth mindset and lifelong learning, ����ý is seeking to leverage technology to streamline the accreditation process; provide valuable, consultative feedback; and reduce burden on schools and volunteers whenever possible. We welcome schools to use AI as a tool in their accreditation journeys.

In line with Guiding Principle 1 in ����ý’s accreditation standards, we expect that ethics and integrity will be paramount in the use of all technology, including generative AI tools. And, in line with Guiding Principle 10 in the standards, all information that schools provide to ����ý should be accurate. Schools must ensure that they use technology as an enabler, not a replacement, for reporting information to ����ý, whether it is in accreditation reports or in periodic surveys, such as the ����ý Business School Questionnaire. Peer review teams will certainly be interested in how schools are embedding AI into their curriculum and how they are preparing learners with this current and emerging technology, consistent with Standard 4.

Continued Commitment to Diversity

The issue of diversity has continued to be a popular topic of conversation, largely due to various legislative actions in the United States that restrict the use of public funds to support diversity efforts at public colleges and universities. Questions center on what an accreditation team can reasonably expect of a school that operates in an area where diversity efforts are stifled by local leaders.

In the 2020 accreditation standards, ����ý’s Guiding Principle 9 relays the Accreditation Council’s expectation related to diversity and inclusion:

Diversity in people and ideas enhances the educational experience and encourages excellence in every business education program. At the same time, diversity is a culturally embedded concept rooted in historical and cultural traditions, legislative and regulatory concepts, ethnicity, gender, socioeconomic conditions, religious practices, and individual and shared experiences. Within this complex environment, the school is expected to demonstrate a commitment to advancing diversity and inclusion issues in the context of the cultural landscape in which it operates. The school fosters awareness, understanding, acceptance, and respect for diverse viewpoints related to current and emerging issues.

This language makes it clear that ����ý views diversity through a global lens, and that each school is expected to interpret and apply diversity within its unique cultural context. The 2020 standards are not prescriptive in how diversity is defined at any school—that is the prerogative of the school. Neither are the standards prescriptive around admission criteria, as this is also the prerogative of the school. Thus, we do not view ����ý accreditation standards as conflicting with U.S. legislation, and we do not expect to make any changes to the standards at this time. ����ý’s core values include a deep and abiding commitment to diversity and equitable access to high-quality education, for everyone.

Accreditation Visits This Year

Schools with 2023–24 visits should be mindful of several focus areas, including visit modality, disclosure of student outcomes to the public, and measuring societal impact.

While the COVID-19 pandemic presented unprecedented challenges globally, business schools demonstrated grace and agility over the past three years in continuing to serve learners through high-quality business education. As the world has now moved out of the most critical pandemic stage, accreditation visits are nearly universally back to a face-to-face modality. However, the lessons we learned about how to conduct high-quality virtual visits will remain with us. Going forward, we have the tools and processes needed to conduct a virtual visit at any time if circumstances necessitate a change of plan. However, departure from a face-to-face visit requires ����ý’s approval in advance.

An area of the standards that schools should pay particular attention to is Standard 6.2, which requires public disclosure of academic program quality supporting learner progression and post-graduation success on a current and consistent basis. This information should be available on the accredited unit’s website, where it is clearly displayed and distinguishable from university amalgamated data. As a reminder from documentation for Standard 6.2, disclosures are not prescriptive but are informed by the school’s mission, strategies, and expected outcomes, and may include post-graduate learner success outcomes, admission data, retention and time-to-degree data, diversity and inclusion advances, particular program emphases, student learning outcomes, rankings data, experiential learning opportunities, meaningful societal impact, or other mission-specific outcomes.

A second area of the standards for schools to closely consider is societal impact. ����ý released a white paper on how to align with the expectations of the 2020 standards in February 2023. Measuring societal impact has also been a popular topic recently, and this paper walks you through how to write an impact statement that provides a roadmap to measuring your school’s societal impact efforts. To learn more, download ����ý and Societal Impact: Aligning With the ����ý 2020 Business Accreditation Standards.